A recent blog by Ralph Frank – ‘TLAs, the FCA, IGCs & TCF. WTF?’ – that I accessed through the excellent Pensions PlayPen group on LinkedIn, got me thinking about IGCs.

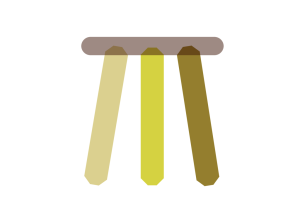

To start with, let’s get the conflict out of the way. I am an independent trustee so this is a bit of a Mandy Rice-Davies moment. I am naturally predisposed to the idea of independent oversight as it is how I make my living. So, bearing that in mind, I trust you will still find my 3-legged stool analogy to be a useful one.

There is always tension in any business between the needs of the owners, the workers and its customers. It is a great business indeed where:

• the owners are happy with their profits & prospects,

• the workers are happy with their pay & conditions and

• the customers are happy with the product, price & service.

My analogy imagines a business as being built on a 3-legged stool, As we all know, for the stool to work it is important that each leg is the same length. If any leg gets too long or too short the whole thing becomes increasingly unstable.

In my analogy the business is the seat that rests on three legs: the owners, the workers and the clients. Any tension is translated to a wobbly stool.

As a business grows it must meet the needs of each party. If it neglects one leg or puts an over emphasis on another, the result will be instability. You can’t run a business for long where:

• your customers don’t like your product, price or service, and/or

• your workers don’t like their pay and conditions, and/or

• your owners don’t like the level of profits or their prospects.

In these conditions change is inevitable. Such change is normally driven by problems not by opportunities.

Now let’s apply this idea to the business of a pension provider. The players are essential the same but in a pension scheme the customer (member) is significantly disadvantaged by two pretty much universal features of pension schemes:

• Firstly – the customer is a step removed from the buying decision in that it was not their decision to choose the particular pension scheme. Whether it is your Grandma buying you a birthday present, or an employer setting up a pension scheme – however good the intention – the buyers interests are rarely perfectly aligned with those of the end-user!

• Secondly – with a pension, it is very difficult to know whether you are happy with the product, price and service.These are issues that experienced professionals argue over: how is a DC pension scheme member expected to know?

I don’t think that it is too controversial to suggest that, in the past at least, many pension scheme members have often been lumbered with a very short leg. Anyone who has worked in the industry for any length of time will have seen pension scheme contracts that have been heavily weighted in favour of almost anyone but the members.

As for being happy with the product, price and service, perhaps the best indicator here is the fact that the average DC pot at retirement is just £25,000 (source: The Pensions Regulator). Whilst there are undoubtedly numerous other factors that feed into poor retirement outcomes, the issue of trust in the pensions system simply cannot be ignored. So, what can be done about this?

Well, there is no shortage of heavyweight players in the pensions market.

- the Department for Work and Pensions (‘DWP’)

- The Prudential Regulations Authority (‘PRA’) promotes safety and soundness of financial firms and seeks to provide protection for policy holders

- The Financial Conduct Authority (‘FCA’) supervises the conduct of over 50,000 financial firms

- The Pensions Regulator (‘tPR’) has 6 laudable statutory objectives

We also have numerous industry bodies and associations. So, it is quite reasonable to ask the question: What role is there for yet another body – the Independent Governance Committee?

The key lies in a very simple yet fundamental point. The DWP, PRA, FCA and tPR by necessity work from the top down – IGCs will work from the bottom up. The role of the IGC will start with the customer – the members of pension schemes. The IGCs will have a clear and simple remit to act in the interest of members

We shall have to wait a while yet for the full rules for IGCs. The consultation period initiated by the FCA, tPR and DWP ended on the 10 October 2014. This asked 31 questions and, if previous consultations are anything to go by, the contributions provided will be reflected in the final rules.

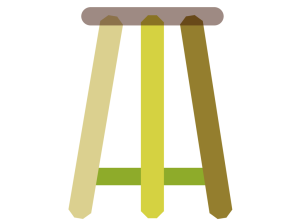

In the meantime, I want to take my three-legged stool analogy a little further.

As a pension scheme grows in size, it moves from being a milking stool to a bar stool. The bigger our stool gets the more it needs something to bind the 3 legs together. Without the proper structures down below the stool soon becomes unstable.

In my analogy, one of the key roles of the IGC is to help bind the legs together. A strong binding allows the legs to get longer and provide a broader base. The IGC is in a good position to do this as it looking up from the bottom. Crucially, it is not part of the business and does not get caught up in the sometimes exciting view from the top. A good pension provider will recognise that a proactive IGC can play an important part in promoting the sustainable growth of the business.

Now, you may well argue that the IGC’s job is to look after the interests of the pension scheme members. I would agree. I am extremely confident that IGCs will be given a very strong remit to perform this function. I would also argue that it is entirely in the members’ interest for their pension provider to be as strong and stable as it can possibly be.

In my opinion, an IGC that views its remit in the very narrowest sense and ignores the other parts of the stool is going to find it difficult to get the best possible outcomes for the members:

- How can members expect good pension outcomes from an unstable pension provider?

- How can you promote a good outcome if the pension provider doesn’t have the financial support and leadership it needs?

- How can you expect good service from a pension provider if the workers are routinely dissatisfied?

Ideally, in order to promote the best interest of members, the IGC will want to work with the business, its owners and it’s workers. Being Independent and looking after the interest of members, does not by necessity put the IGC in opposition to the interests of the business. This is far from a ‘them-and-us’ situation. The IGC will have to hold the business to account but this does not have to be translated in to some form of permanent conflict.

Whilst the whole idea of the IGC is still in its infancy and time will ultimately tell us whether they will prove to be a good idea, I have every confidence that they will be a force for good in the pensions market. In my opinion it is essential for all parties to start off by concentrating on their common interests. It will be important to use the early days to build the levels of mutual trust that will be required to build sustainable solutions for the benefits of members if conflicts start to arise.

Jonathan Reynolds

PS – there is no connection between the writer (who is often referred to as Jon – amongst other things) and John Reynolds – the man responsible for the consultation. This is pure coincidence.